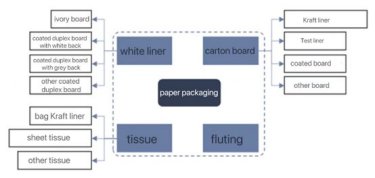

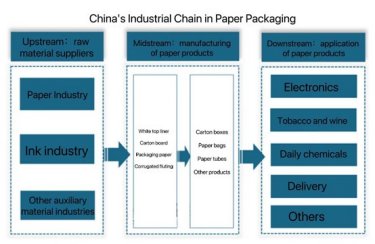

Paper packaging is the world's largest amount of packaging materials. In recent years, China's packaging paper industry production volume has risen steadily. From 2015 to 2021, China's packaging paper production increased from 6.65 million tons to 7.15 million tons, with an average annual compound growth rate of 1.22%.

IV. Analysis of the development status of China's paper packaging industry

1. Analysis of business status

According to the data of the China Packaging Federation, in 2021, the scale of the national packaging industry has reached 1204.181 billion yuan, of which the scale of the paper packaging field has reached 319.203 billion yuan, an increase of 10.65% year-on-year, accounting for 26.51% of the total scale of the packaging industry, and the industry CAGR from 2016 to 2021 has been -0.9%; The scale of 2022H1 paper packaging reached 155.862 billion yuan, an increase of 1.48% year-on-year, and the total profit of the industry was 4.985 billion yuan, down 14.06% year-on-year, and the decline in profit was mainly due to the increase in raw material prices in the first half of 2022.

2. Analysis of export status

From the perspective of exports, the cumulative export volume of the national paper and paperboard container industry in 2022H1 was 4.606 billion US dollars, a year-on-year increase of 25.44%. Since 2019, the growth rate of export volume has been higher than that of China’s paper packaging industry, and its domestic paper packaging enterprises continue to benefit from the growth demand of overseas paper packaging market.

From the perspective of export distribution, the top five countries and regions in terms of export value in 2022H1 are the United States (23.80%), Australia (5.10%), the United Kingdom (4.20%), Hong Kong (4.09%), and Vietnam (4.03%). In 2022H1, the growth rate of exports to Singapore (157.1%), Malaysia (62.1%), the United States (31.0%) and Germany (28.3%) was higher than that of total exports (25.44%).

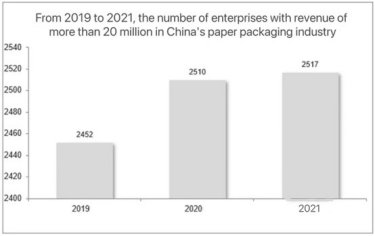

3.Number of enterprises

In 2020, there were only 20 paper packaging enterprises with annual revenue of 1 billion in China, among which the top 3 enterprises reached 10 billion. In 2021, there were 2,517 enterprises with annual revenue of more than 20 million yuan in paper packaging. The distribution of paper packaging industry presents a long tail phenomenon, mainly due to the low barriers of paper packaging industry and the difficult assessment of packaging quality. Small workshops in various regions still occupy a large market share with the cost of cheap and low-quality pulp and the low labor costs in the third- and fourth-tier cities. In recent years, under the supervision of environmental protection packaging policies, the operating costs of some small workshops have increased, accelerating the liquidation of small and medium-sized enterprises in the industry.

From 2019 to 2021, the number of enterprises with revenue of more than 20 million in China's paper packaging industry